India’s protein nutrition market is undergoing a fundamental transformation.

What was once considered a niche category catering primarily to athletes and fitness enthusiasts is rapidly evolving into a broader wellness and nutrition segment. Rising health awareness, increasing disposable incomes, and growing interest in preventive healthcare are driving protein consumption across a much wider consumer base.

With the market projected to grow from approximately $4.7 billion in FY2025 to nearly $17.2 billion by FY2034 at a 14.7% CAGR, protein is no longer just a fitness supplement – it is increasingly becoming part of everyday nutrition.

Protein Is Moving Beyond the Gym

Historically, protein supplementation in India was largely associated with bodybuilding and sports nutrition. Today, India’s protein consumption landscape is undergoing a significant transformation, driven by rising health awareness, increasing disposable incomes, and a growing focus on preventive wellness.

Once viewed primarily as a specialized supplement for athletes and bodybuilders, protein is increasingly being adopted as an essential component of everyday nutrition. This shift is expanding the consumer base beyond fitness enthusiasts to include families, working professionals, women, and health-conscious individuals seeking benefits such as weight management, active aging, and overall well-being.

Simultaneously, innovation in product formats is making protein consumption more convenient and accessible than ever before. While protein powders continue to remain relevant, the emergence of protein bars, ready-to-drink beverages, snacks, and functional foods is enabling brands to integrate protein into everyday consumption occasions, further accelerating mainstream adoption across India.

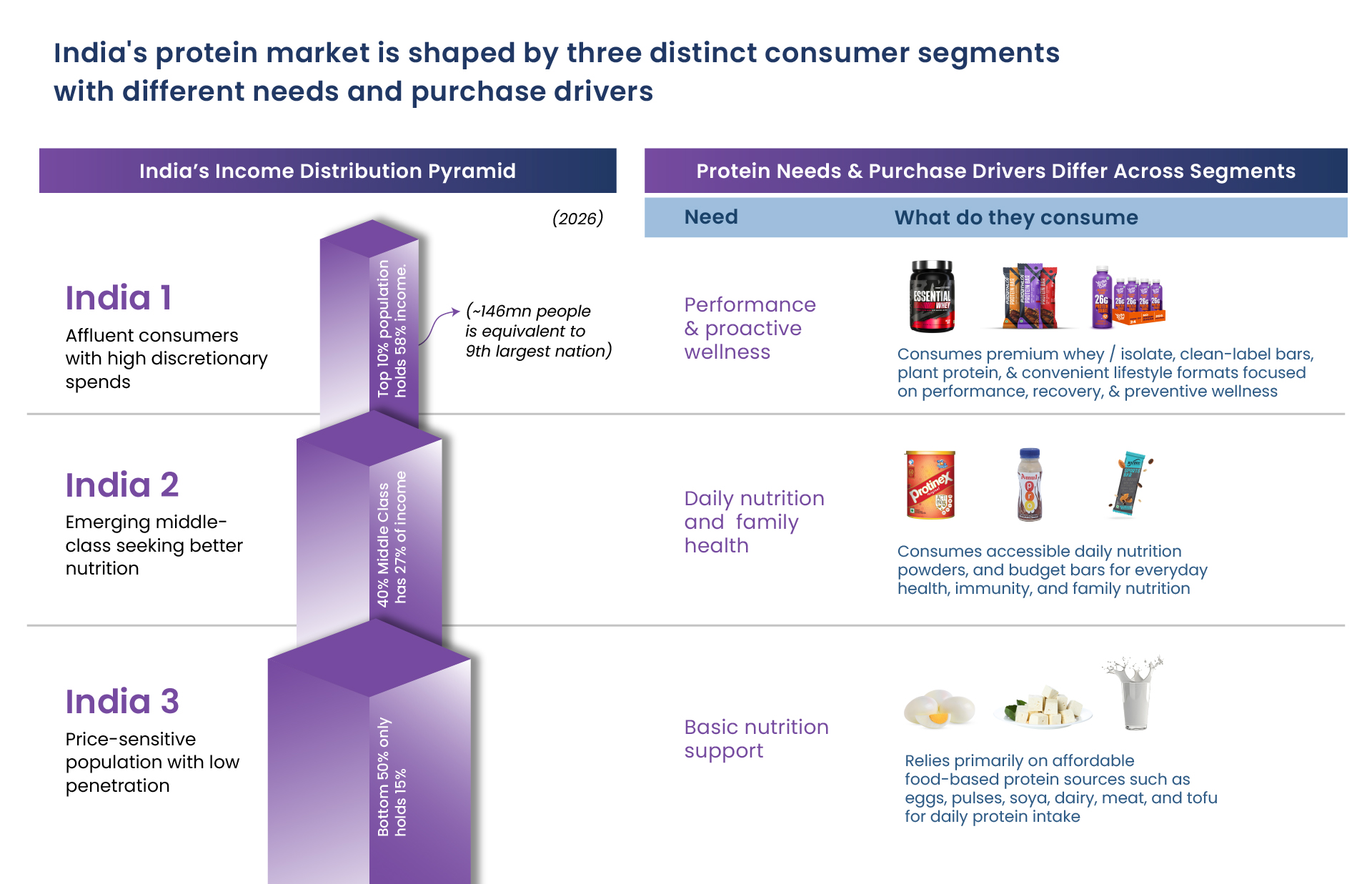

One Market, Three Indias

The protein opportunity in India is far from homogeneous.

Consumer adoption is being shaped by three distinct segments, each with different purchasing power, motivations, and consumption behaviours.

Affluent consumers are increasingly seeking premium whey, isolates, clean-label products, and plant-based formulations that support performance and proactive wellness. Emerging middle-class consumers are driving demand for affordable daily nutrition products focused on family health and balanced nutrition. Meanwhile, a large price-sensitive population continues to rely on traditional protein sources such as dairy and eggs to meet basic nutritional needs.

This segmentation is creating multiple growth opportunities across both premium and mass-market price points.

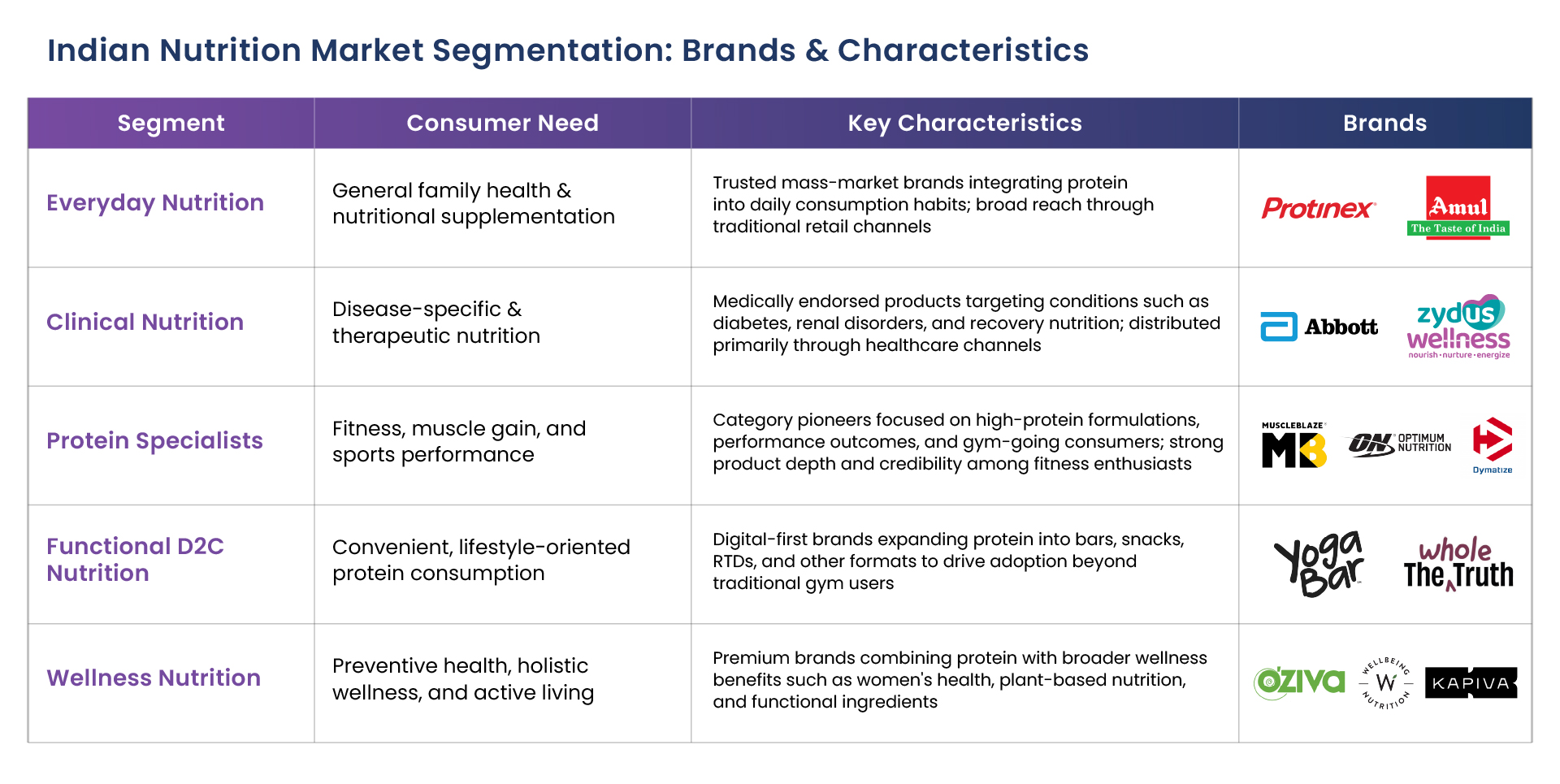

The Market Is Fragmenting Around Consumer Needs

As adoption broadens, the competitive landscape is becoming increasingly specialized.

Rather than competing within a single “protein supplement” category, brands are positioning themselves around distinct consumer use cases. These include everyday nutrition, clinical nutrition, sports performance, functional nutrition, and holistic wellness.

While specialist sports nutrition brands continue to dominate the fitness segment, some of the fastest-growing opportunities are emerging in wellness-oriented and lifestyle-driven consumption occasions. Consumers are increasingly seeking products that align with broader health goals rather than purely muscle-building outcomes.

This shift is expanding the category’s addressable market and creating room for new business models and product innovations.

Online & Offline Channels Are Playing Different Games

The evolution of the protein category is also reshaping distribution dynamics, with online and offline channels serving distinct but increasingly complementary roles.

Offline channels – including pharmacies, nutrition stores, modern trade outlets, supermarkets, and neighborhood grocery stores – continue to play a critical role in building trust and facilitating first-time product trials. For many consumers, particularly in Tier 2 and Tier 3 cities, protein remains a relatively new category where recommendations from pharmacists, fitness trainers, or store staff can significantly influence purchase decisions. Established brands such as Protinex and Ensure have long leveraged these channels to build credibility and drive adoption among families and health-conscious consumers.

Online channels, meanwhile, are emerging as the primary engine for product discovery, consumer education, and repeat purchasing. E-commerce marketplaces such as Amazon and Flipkart, brand-owned D2C websites, e-pharmacies, and increasingly quick-commerce platforms allow consumers to compare products, access a broader assortment of brands, read reviews, and subscribe for convenient replenishment. For digital-first brands like Whole Truth, MuscleBlaze, and Oziva, online channels have also become powerful tools for community building, personalized engagement, and data-driven customer retention.

The rise of quick-commerce is further blurring traditional channel boundaries. Products that were once planned purchases are increasingly becoming on-demand wellness essentials, creating new opportunities for impulse purchases and faster replenishment cycles.

As the market matures, winning brands will not view online and offline as competing channels. Instead, they will leverage offline presence to build trust and trial while using digital ecosystems to drive engagement, retention, and lifetime customer value. The brands that successfully orchestrate both channels across the consumer journey will be best positioned to capture the next wave of category growth.

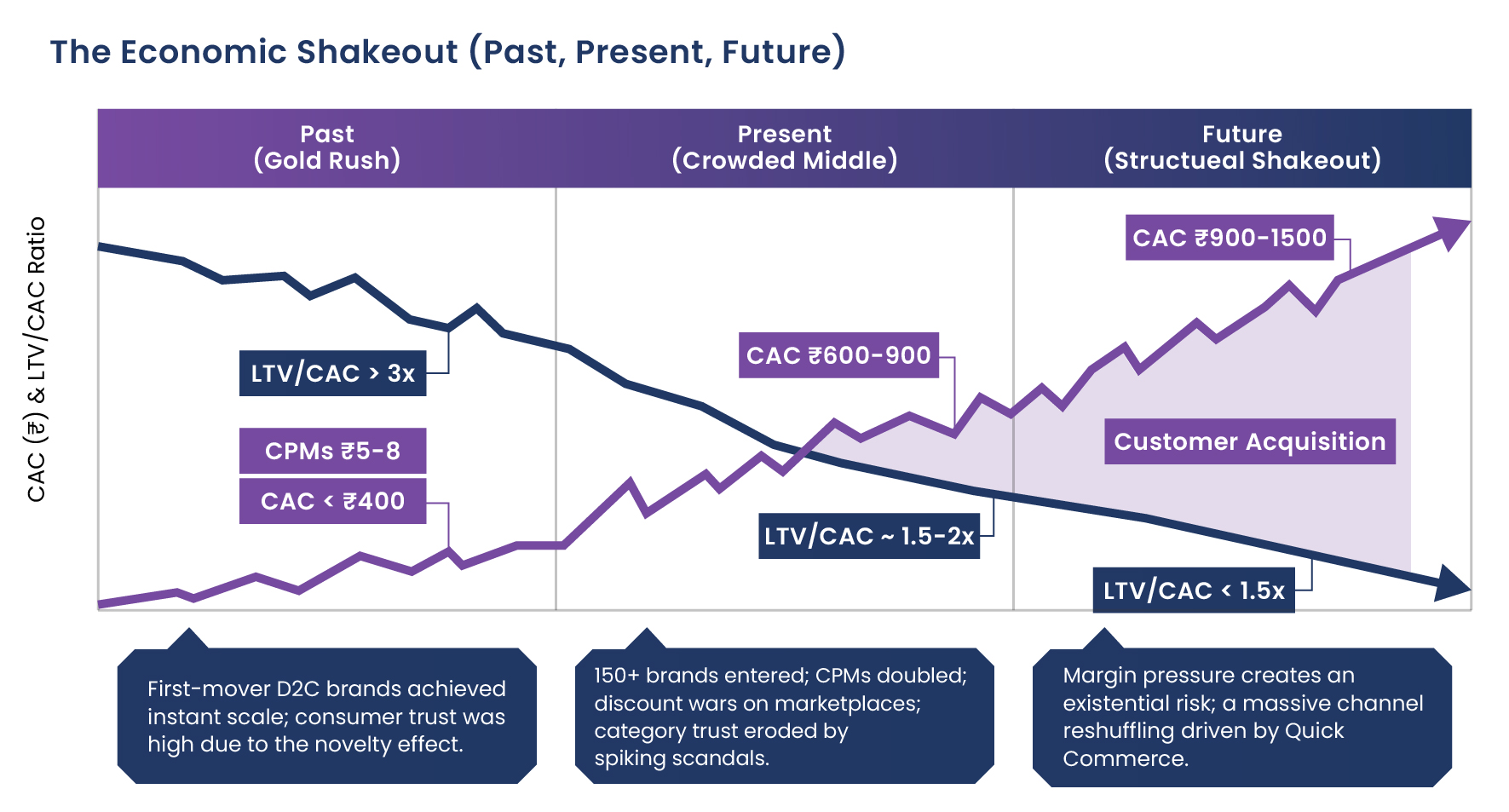

The Next Challenge: Economics

The industry’s biggest challenge may no longer be demand generation – it may be profitability.

Low barriers to entry have attracted more than 150 brands into the category, intensifying competition and increasing customer acquisition costs. What was once a relatively efficient growth environment has become significantly more crowded, with brands competing aggressively through discounts, promotions, and digital advertising.

As acquisition costs continue to rise, sustainable growth will increasingly depend on retention, operational efficiency, and strong unit economics.

The industry appears to be approaching a structural shakeout where scale alone may not be enough to win.

What Will Separate Winners From Everyone Else?

The next phase of value creation in India’s protein market will likely be defined by three factors.

First, brands must focus on retention and habit formation rather than relying solely on customer acquisition. Repeat purchasing will become a critical driver of long-term profitability.

Second, companies will need to build organic consumer demand through content, community engagement, and brand trust instead of depending exclusively on paid marketing channels.

Third, margin discipline will become increasingly important as quick-commerce and evolving distribution models place additional pressure on profitability.

The market’s future winners will not necessarily be those that grow the fastest. They will be the brands that combine consumer relevance with sustainable economics.

Closing Thoughts

India’s protein nutrition market is entering a new chapter.

The opportunity remains significant, supported by favorable demographic trends, rising health awareness, and expanding consumer adoption. However, the basis of competition is shifting. Success is moving beyond product availability and customer acquisition toward retention, differentiation, and profitability.

For brands, investors, and industry participants alike, the question is no longer whether the market will grow. The more important question is which companies can build enduring businesses as protein evolves from a niche supplement category into a mainstream pillar of everyday nutrition.

Insights That Drive Impact

Healthcare is evolving faster than ever — and those who adapt are the ones who will lead the change.

Stay ahead of the curve with our in-depth insights, expert perspectives, and a strategic lens on what’s next for the industry.